A recent incident involving Mr. Jawaid Alam, a 75-year-old retired police officer, has raised alarming concerns about the alleged data leak from the State Bank of India (SBI). Despite SBI’s promises of security and fair treatment, Mr. Alam’s story questions the integrity of the banking system and its ability to safeguard customer information.

Background of the Incident

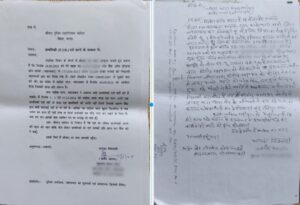

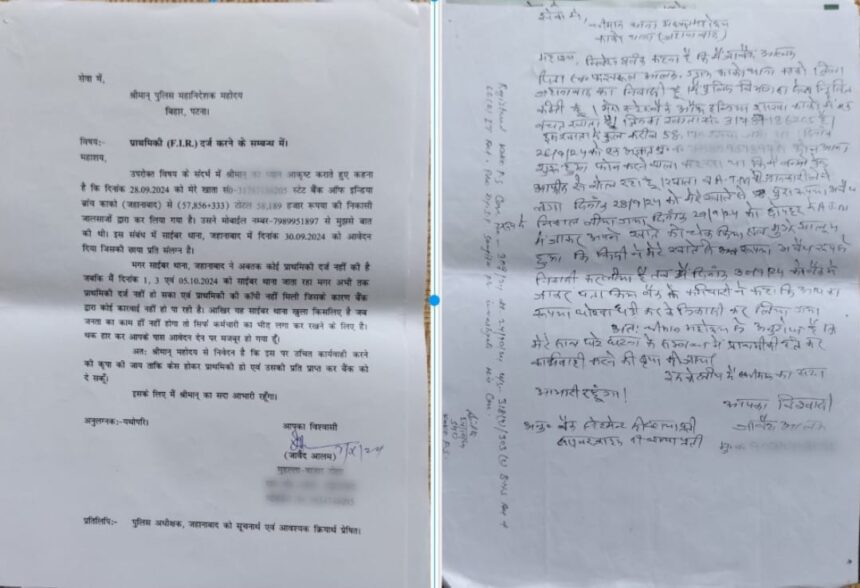

Mr. Jawaid Alam has been a devoted SBI customer for three decades, trusting the bank with his savings and sensitive information. The incident took a distressing turn when Mr. Alam reportedly fell victim to a fraud scheme that involved unauthorized transactions from his account. Alarm bells went off when he realized that not only were his funds compromised, but his data appeared to have been leaked, potentially exposing him to ongoing threats.

The retired police officer’s report highlights a pattern that is increasingly becoming a recurring issue among bank customers. The lack of effective measures to protect sensitive information raises a myriad of questions regarding how such data leaks can occur within one of the country’s largest banks.

SBI’s Promises and Growing Concerns

The State Bank of India has, for years, positioned itself as the “Banker to Every Indian,” emphasizing its commitment to safeguarding customer information. Their policies promise fair treatment, transparency, and non-discrimination. However, Mr. Alam’s experience challenges these claims, suggesting a gap between promise and reality.

As customer confidence wanes, analysts express concerns that this may not be an isolated incident. Reports of data breaches and account compromises have sparked debate about the safety measures employed by banks across India, particularly regarding customer privacy and data security.

The Larger Implications for Banking Security

Mr. Alam’s case could signify a larger problem within India’s banking sector. If a loyal customer with a clean financial history can fall victim to such fraud, it implies systemic vulnerabilities that could impact thousands of unsuspecting individuals. The potential for a data leak at a financial institution like SBI raises concerns about the protective measures in place to safeguard against cyber threats.

Experts argue that the banking system needs a comprehensive review of its cybersecurity protocols. Increased vigilance and technological upgrades are necessary to ensure that the sanctity of customer data is preserved. The fallout from such incidents could undermine public trust and lead to increased scrutiny of banking operations and regulatory standards.

Why This Matters

The implications of Mr. Alam’s experience extend beyond one individual, highlighting a pressing issue that impacts the financial security of countless citizens. In a democratic society where trust in public institutions is paramount, ensuring the safety of personal information must be a priority for banks. As India rapidly digitizes its banking sector, maintaining robust data security becomes critical for economic stability and consumer confidence.

This incident could catalyze a broader conversation about regulatory reforms and the need for increased accountability among financial institutions. As citizens demand transparency and accountability, the banking system must adapt and evolve to safeguard against emerging threats.

Frequently Asked Questions

What happened to Mr. Jawaid Alam?

Mr. Alam, a 75-year-old retired police officer and a long-time SBI customer, reportedly fell victim to fraud resulting from an alleged data leak, leading to unauthorized transactions from his account.

How does SBI claim to protect customer information?

SBI emphasizes transparency, fairness, and the protection of financial information as part of its Depositors’ Rights policy, positioning itself as a secure banking option for all Indians.

What are the implications of this incident for other bank customers?

This incident raises concerns about potential vulnerabilities in banking systems that may affect many customers, pointing to a need for improved cybersecurity and protective measures across financial institutions.

Why is customer trust important for banks?

Customer trust is essential for the stability of financial institutions. If clients lose confidence in banks’ ability to protect their information, it could lead to decreased patronage and demand for significant regulatory reforms.