The Indian money market serves as the primary channel through which banks, financial institutions, and large corporates access short-term funding. The issuance of certificates of deposit (CDs) by banks and commercial papers (CPs) by financial and corporate entities constitutes its core supply, with mutual funds emerging as the leading investor segment.

Recently, the market has transitioned into a phase characterized by increased CD issuance, significantly wide spreads, a sharp decline in corporate CP supply, and persistent low liquidity in the secondary market. Unlike the stresses observed during the post-IL&FS period (2018–19), the current situation is not driven by credit concerns.

This environment is shaped by various factors, including changes in investor behavior, regulatory liquidity requirements for banks, seasonal trends in mutual funds, and constraints in portfolio construction within the mutual fund industry.

CD Issuance

Since mid-2023, system liquidity has gradually tightened following a period of surplus post-COVID. In the meantime, credit demand has rebounded meaningfully. Bank credit, which dropped to 9 percent in May 2025, surged to about 15 percent by mid-April this year, leading many banks to revise their credit growth forecasts for FY27.

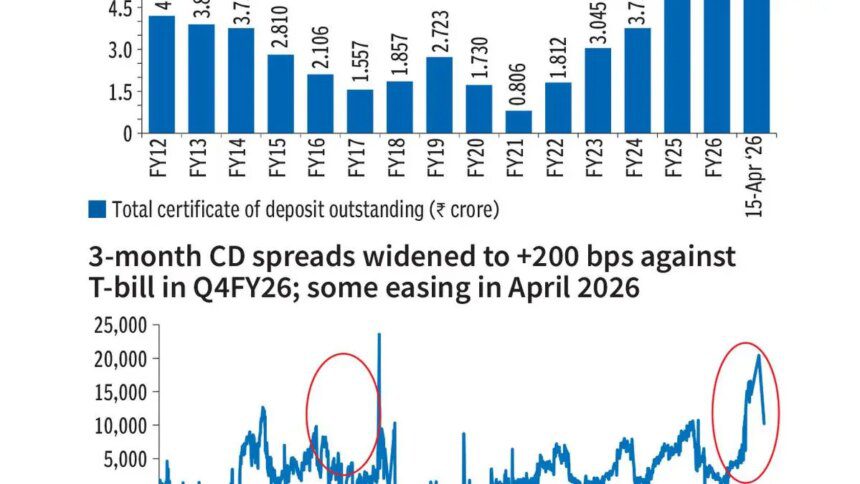

As credit growth outpaced deposits, banks increasingly utilized CDs as a tool for wholesale funding. Outstanding CDs nearly doubled from approximately ₹3 lakh crore at the beginning of 2023 to almost ₹6 lakh crore by January and about ₹7 lakh crore by April. This trend was further driven by quarter-end balance sheet management and heightened loan demand.

CD spreads relative to 3-month T-bills widened significantly. After softening in the first half of 2025 due to policy rate cuts, spreads expanded from 30–40 basis points in mid-2025 to 75–80 basis points by year-end, peaking at 220 basis points in February-March. While these spreads eased to 100-120 basis points in April due to seasonal adjustments, they remain markedly elevated year-on-year. Structural mismatches between supply and demand persist.

CD Supply

While banks actively issue CDs, corporate CP issuance has slowed. Many corporates find that borrowing from banks—linked to external benchmark lending rates, such as T-bill formulas—is more cost-effective than issuing CPs.

Weak Appetite

Mutual funds continue to be the primary investors in CDs and CPs; however, their available assets under management (AUM) for these instruments have not kept pace with increasing supply. Regulations from the Securities and Exchange Board of India (SEBI) regarding duration and credit categories restrict fund flexibility during volatile periods.

For instance, liquid funds are prohibited from buying instruments with maturities beyond 91 days, while overnight funds can only invest in one-day instruments like tri-party repos (TREPS). Equity and hybrid funds typically maintain cash for margins but cannot utilize it for longer-tenor CDs or CPs. This scenario has led to a discrepancy wherein headline liquidity, notably from the large overnight TREPS market, does not accurately reflect mutual funds’ capacity to invest in money market instruments.

AUM Reallocation

Tax changes for debt mutual funds in Budget 2023 have significantly diminished the post-tax attractiveness of such funds for retail investors, shifting flows towards equity and hybrid categories. Consequently, debt fund inflows have become largely institutional, resulting in concentrated AUM growth within overnight funds primarily utilized for corporate treasury management. Meanwhile, medium- and long-duration debt funds have stagnated or experienced outflows, contributing to AUM volatility and reduced demand for CDs and CPs.

Bank Bulk Deposits

As banks compete for both current/savings account (CASA) and term deposits, they are also mobilizing bulk deposits, which directly compete with mutual fund liquid schemes. Bulk deposits provide stable returns devoid of mark-to-market volatility, attracting many corporates, thereby diverting flows from mutual fund schemes that typically invest in CDs.

Illiquidity

Despite significant outstanding volumes, secondary trading in CDs and CPs remains limited and primarily focused on short residual maturities and top-rated issuers. Long-term investors such as insurers and provident funds generally avoid this market segment. Banks are mainly involved for liquidity coverage ratio (LCR) management, leaving mutual funds as the primary active traders in the secondary market. Synchronization in redemption patterns among fund houses leads to simultaneous selling pressure, which diminishes bid-side depth and encourages a bias toward diversified, conservative portfolios. The CP market is particularly illiquid, necessitating additional spreads to compensate for liquidity risk.

Seasonal Patterns

Seasonality also plays a role in influencing short-term rates. Each March, and at other quarter-ends, corporates withdraw 20–25 percent of liquid fund AUM for tax and balance sheet necessities. These funds typically re-enter the market in April, lowering short-term yields. Ahead of March, mutual funds postpone purchases of 3-month papers to mitigate reinvestment risk, resulting in tenor mismatches and temporary spread spikes despite otherwise stable system liquidity.

CD Spreads

Some reduction in CD spreads is anticipated following the March redemption cycle. However, sustained credit growth indicates ongoing funding needs for banks. With short-tenor CD rates on the rise, banks may begin to favor longer-tenor infrastructure and Tier II bonds, supported by renewed infrastructure-eligible assets. This shift could gradually alleviate pressure on CD spreads.

Elevated CD spreads highlight the balance of strong bank funding needs against muted institutional demand and ongoing secondary market illiquidity. In the absence of broader market participation or new liquidity mechanisms, the existing supply-demand mismatches are likely to continue influencing short-term rates in India’s money market.